HPML loans are defined as “consumer-purpose, closed-end loans secured by a consumer’s principal dwelling that have an APR equal to or greater than the Average Prime Offer Rate (APOR published by the Fed and posted on the Federal Financial Institutions Examination Council web site) by 1.5 percentage points for first-lien loans, or 3.5 percentage points for subordinate-lien loans for a comparable transaction.”

This website imports the .csv file from Freddie Mac and then calculates the maximum APR available to avoid being classified as an HPML type loan. We then display the past five weeks of these values, for both first and subordinate loans ... and for standard ARMs and Fixed loans. There is even a "custom" calculations for those loans that are not covered with the standard pages (just select the number of years desired and calculate).

This chart is used by many banks to make sure that the APR rate (and rules that follow) is not going to be considered as HPML.

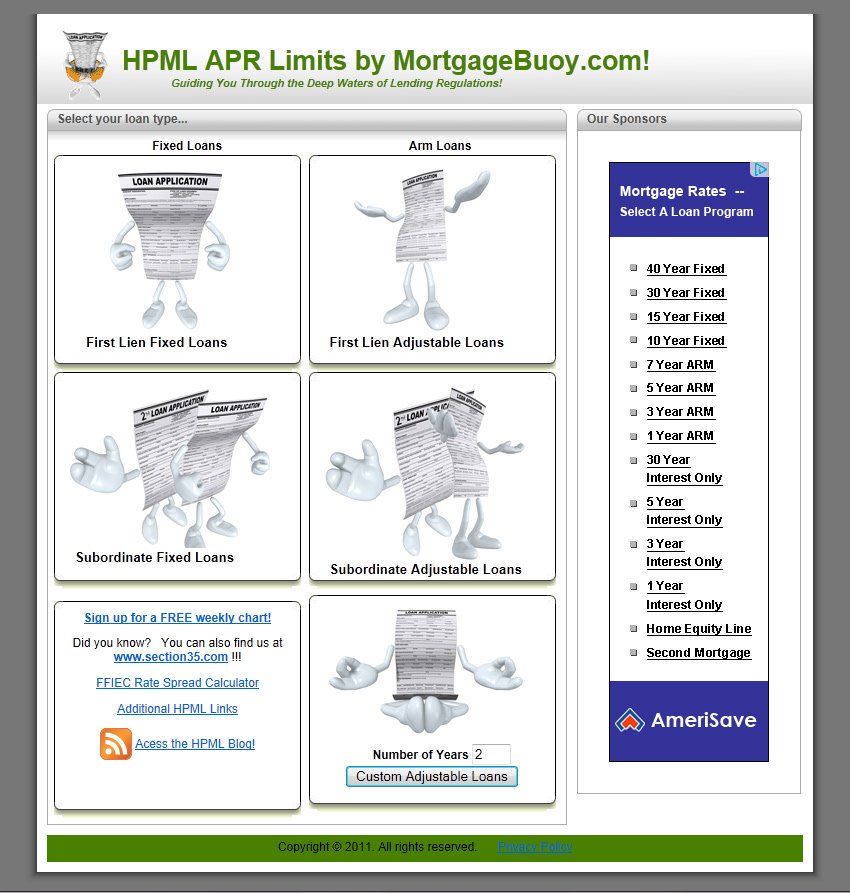

Main page for user to select a loan lien position and loan type (or select a custome adjustable loan type).

Example of Fixed Rate Loan chart (4/13/2012)

Example of max APRs for Subordinate Arm Loan (4/13/2012)

Customers are able to sign up for a free e-mail of the weekly chart.