INVERSITY CASE STUDY

Envisioning a future where democratic financial literacy and investing is accessible for everyone

How the Service Design methodology enabled the development of a service to teach financial literacy in a simple and engaging way, while at the same time offering possibilities for actual investment.

OVERVIEW

In 2020, the Organization for Economic Co-operation and Development (OECD) published a study on financial literacy amongst adults across 26 countries.

"The results provide information about financial literacy that go beyond knowledge, covering aspects of financial behavior and attitudes. Trends of financial inclusion are reported. Particular attention has been paid to elements that provide insights into the financial resilience of individuals, an important characteristic that is proving very pertinent during times of economic and financial volatility." ¹

Some key findings from the study suggest the following:

• Financial literacy is low across the sampled economies

• Less than half of the respondents purchased a financial product or service

• Large groups within many economies have limited financial resilience

• Financial stress is common

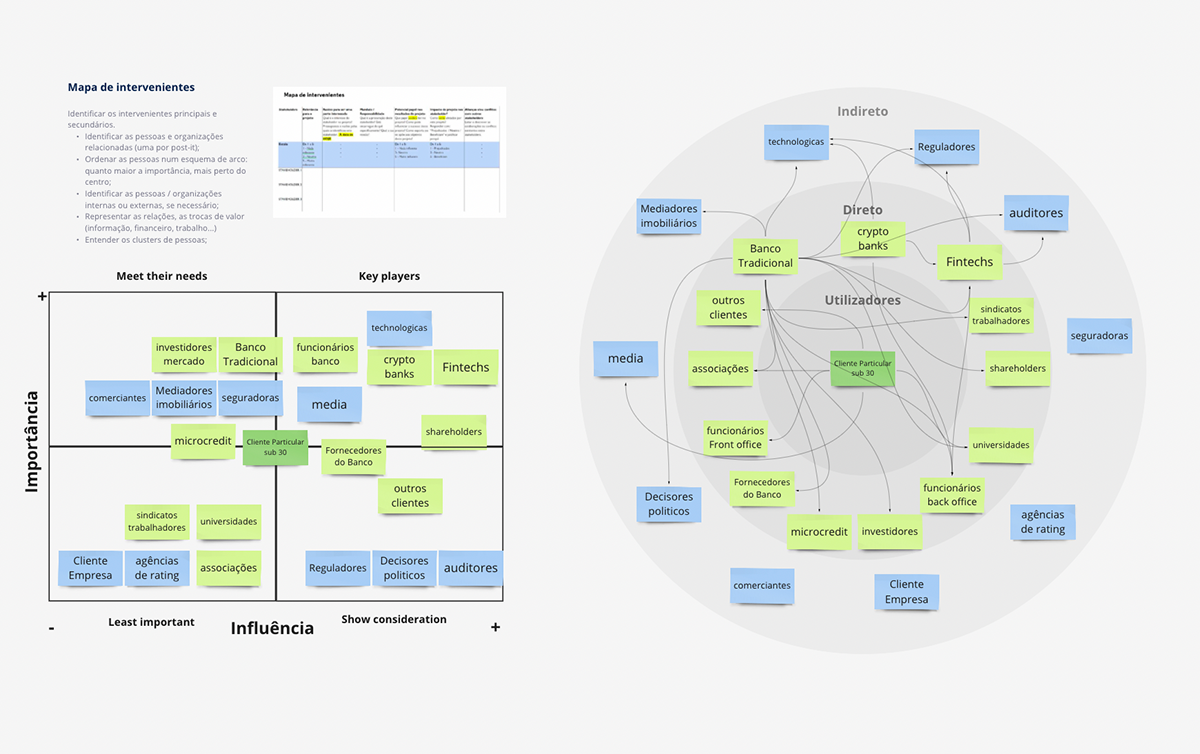

The challenge presented to our team was the development of a service in the banking area, especially focused on young digital natives. Initially, the service's target audience was to be focused on young people under 30, but as we investigated and interviewed more and more people, we realized that what we wanted to create should have a wider reach and impact.

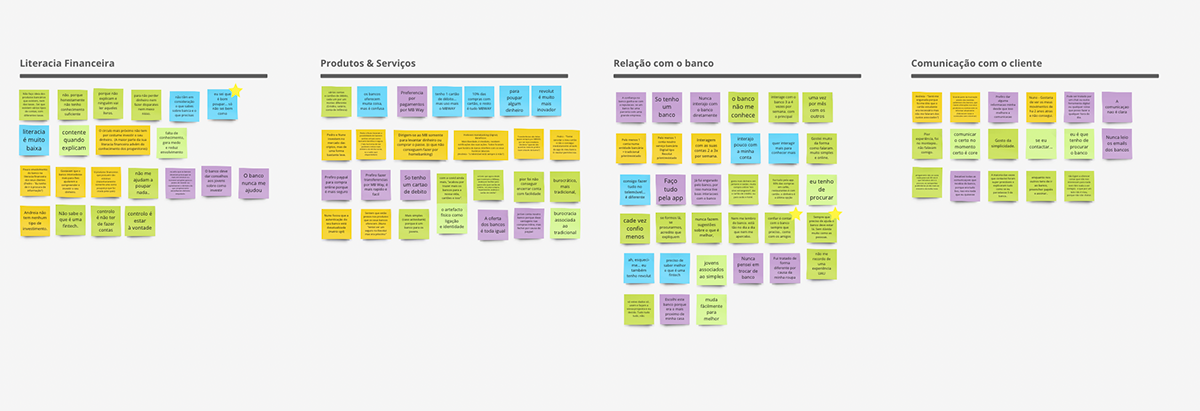

Once we started to explore the relationship between different people and their banks, we quickly realized that there is a large gap between their goals and what they are actually receiving from their banks. Most interviewees reported having a somewhat unstable relationship with their money, especially concerning specific knowledge on how to invest and generate more capital in the future, thus feeling helpless and insecure in this domain of their lives.

Many of these people also reported feeling that banking institutions do not know how to communicate with them in a way that clarifies the available offer of financial products.

The lack of financial literacy seems to spring from a cycle of fear and distrust generated from banking institutions that do not understand how their clients feel towards them, don't know how to communicate their offer, and persist in using technical language that alienates the common user from connecting with the process and mindset of investing, including its risks and benefits.

DISCOVER

One of the most interesting pieces of information we came across during our research was Finastra's study "Redefining finance for good - The journey to financial empowerment " - an ethnographic global study that uncovers how people around the world feel about money, and the relationship they want to have with their financial institutions.

For many people, banking is a very emotional subject. Many respondents found it difficult to describe. Some said it was simply “not for them”, while others did not feel competent to talk about it. There is a strong sense of not understanding banking, because banks talk in a language that people do not relate to. Banks use small print and complicated language to describe their products and services or to talk about interest rates.

As a consequence, people tend to ignore their bank and its messages. There is a sense of “ignorance is bliss”, i.e. I don’t read communications from the bank and I avoid going to the branch. Banking is something that people put off doing. ²

Here’s what we learned about the study:

Knowledge

People first need knowledge about their bank: a practical understanding of what is available to help them manage their money so they can have a sense of control.

People first need knowledge about their bank: a practical understanding of what is available to help them manage their money so they can have a sense of control.

Control

With a sense of control comes a feeling of freedom: the independence and peace of mind that gives the individual the power to enjoy their finances.

And at the heart of everything is personalization, meaning that the individual is at the center of their financial situation, not their bank.

With a sense of control comes a feeling of freedom: the independence and peace of mind that gives the individual the power to enjoy their finances.

And at the heart of everything is personalization, meaning that the individual is at the center of their financial situation, not their bank.

Freedom

The combination of knowledge and control gives people the freedom to make informed decisions about where to invest and how to do it.

The combination of knowledge and control gives people the freedom to make informed decisions about where to invest and how to do it.

Empowerment

The combination of knowledge, actionable tools and the freedom to choose makes people feel empowered in their choices, thus creating a feeling of financial well-being.

The combination of knowledge, actionable tools and the freedom to choose makes people feel empowered in their choices, thus creating a feeling of financial well-being.

“When people have knowledge, control and freedom, they can plan, design and automate the financial actions in their day-to-day lives.

This creates financial empowerment: the feeling that people can either fulfil their financial goals or comfortably work towards them.”

This creates financial empowerment: the feeling that people can either fulfil their financial goals or comfortably work towards them.”

People want banking to be done

“My way, within my limits and according to my timings”.

“My way, within my limits and according to my timings”.

DEFINE

After the interviews, we were able to define our target persona and better understand their frustrations. It has become evident that personalization is something that is little explored by traditional banks and that the way they communicate with their customers makes them feel alienated from the industry.

When asked about financial products, most of them did not know much about the available offer and reported having fear of exposing their money to situations they did not control or understood.

"I have no idea about the banking products that exist, nor of the fees. I know that there are different types of accounts, with different taxes."

Confidence and transparency seem to be a big topic as well. Most interviewed people reported not having a close relationship with their financial institutions because of mistrust and fear of being taken advantage of.

"I felt cheated because I was told that the student card was needed but they didn't tell me about the associated costs."

On customer communication, it seems that traditional banking has a long way to go. Communication is too technical, impersonal and massified.

“I deactivated all the communications I received from the bank, because it was all garbage, it was nothing that I wanted to look at.”

Interestingly enough, talking about the future of banking, virtually everyone agrees that the banks have made an effort to digitize their products and communication.

However, there is always a trade-off between personalization and privacy. Some interviewees agree that they would disclose more personal data if that would translate into a better understanding of their needs and interests, while others reported some concerns about it.

“A bank of the future is a bank that adapts to my habits and immediately gives me the information I want.”

“They could use tools that analyze investment profiles based on their habits and personal information.”

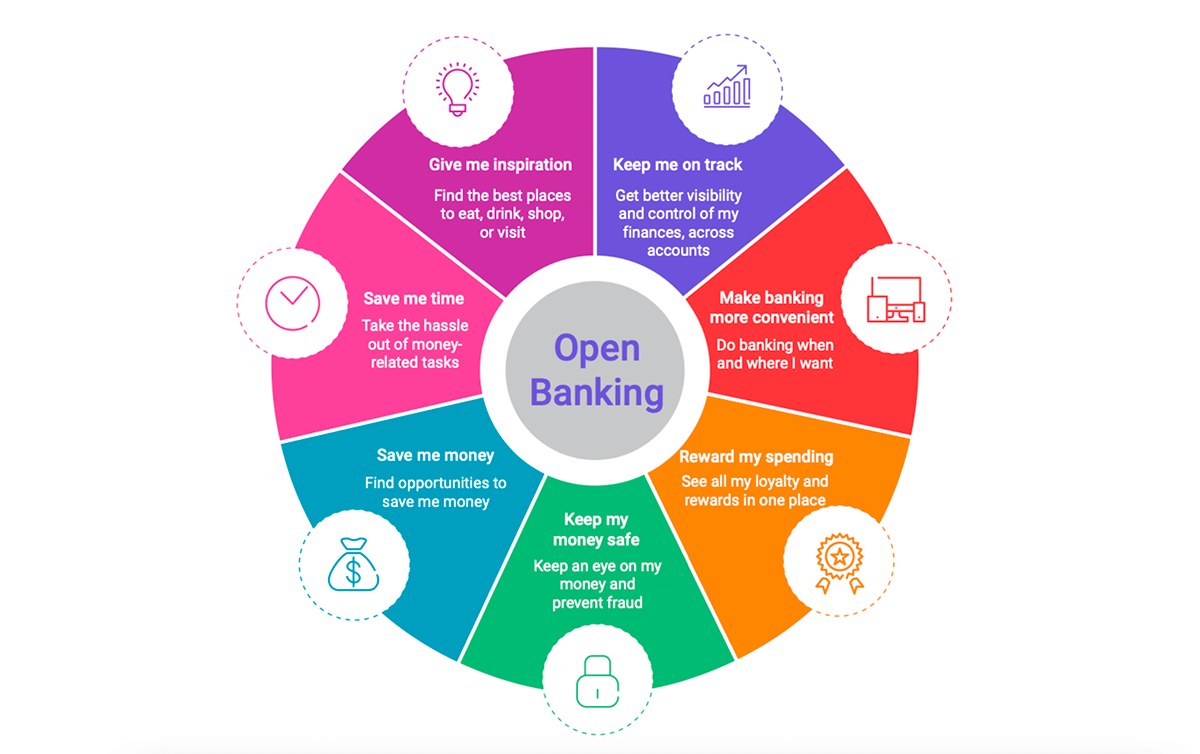

One expert user focused on the decentralization of banking as a way forward into the future, which led us to explore open banking and its potential to address some of these issues.

“As Open Banking grows, it has become a catalyst for the proliferation of APIs. Increased API connectivity between banks and third-party firms is driving innovative and collaborative partnerships, enabling banks to leverage their data and infrastructure to provide new services at a lower cost, and to unlock new opportunities.

Open APIs have become the essential component of digital strategies and the primary way to grow an ecosystem. They are the critical technology enabler for application integration, Banking-as- a-Platform, innovation, and most importantly, customer connectivity.

While the banking industry is rightly excited about Open Banking, consumers haven’t heard of it, therefore they have no awareness of the benefits it could potentially offer. When they discover players that take advantage of Open Banking, they do so via influencers or opinion leaders. It is never their banks that are spreading the Open Banking message.” ²

The most interesting part of this equation is the fact that some key people move through these topics with ease and confidence. Financial literacy influencers create their own content on YouTube, Discord or Reddit and have small communities of followers who trust them and follow their advice.

HOW MIGHT WE...?

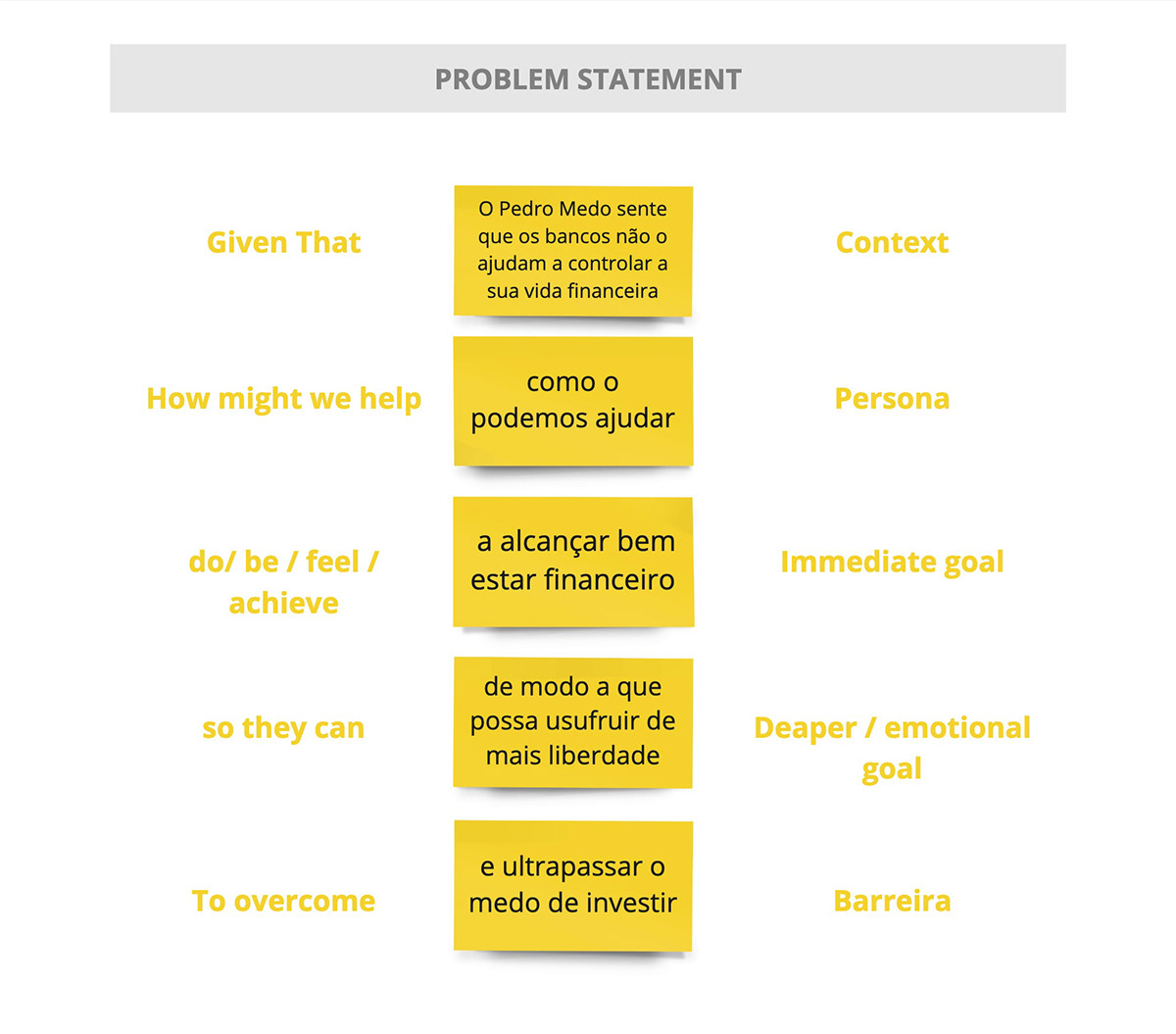

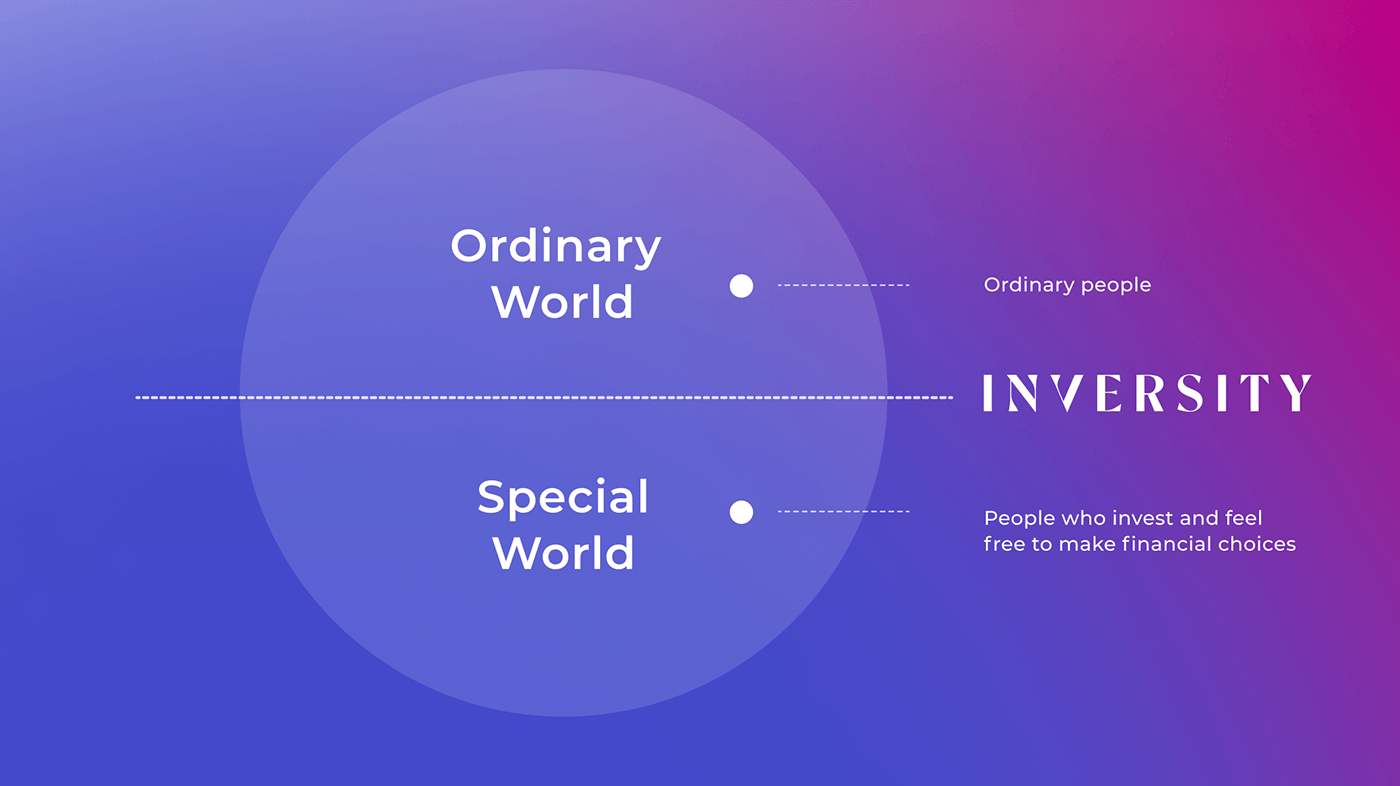

Given that users feel that financial institutions do not help them control their financial lives, how might we help them achieve financial well-being so they can enjoy more freedom and overcome the fear of investing?

Once the problem statement was clear, we understood we were on a journey to financial empowerment for future users.

DEVELOP

When we created the user's journey, we wanted to highlight the frustration peak where the user goes to the bank to learn more about investments and is faced with a world of complexity.

Starting to design a service that would respond to this disappointment, we conceived a concept based on a service that would bridge the gap between financial products from different banks and the user.

The main value proposition of the service would be that only financial products that the user could understand would be suggested for him or her to purchase.

For this, it would be necessary to create courses and learning paths in different areas (ETFs, Insurance, Equities, Digital Currencies...) that would allow the user an intuitive and progressive immersion in the world of financial products.

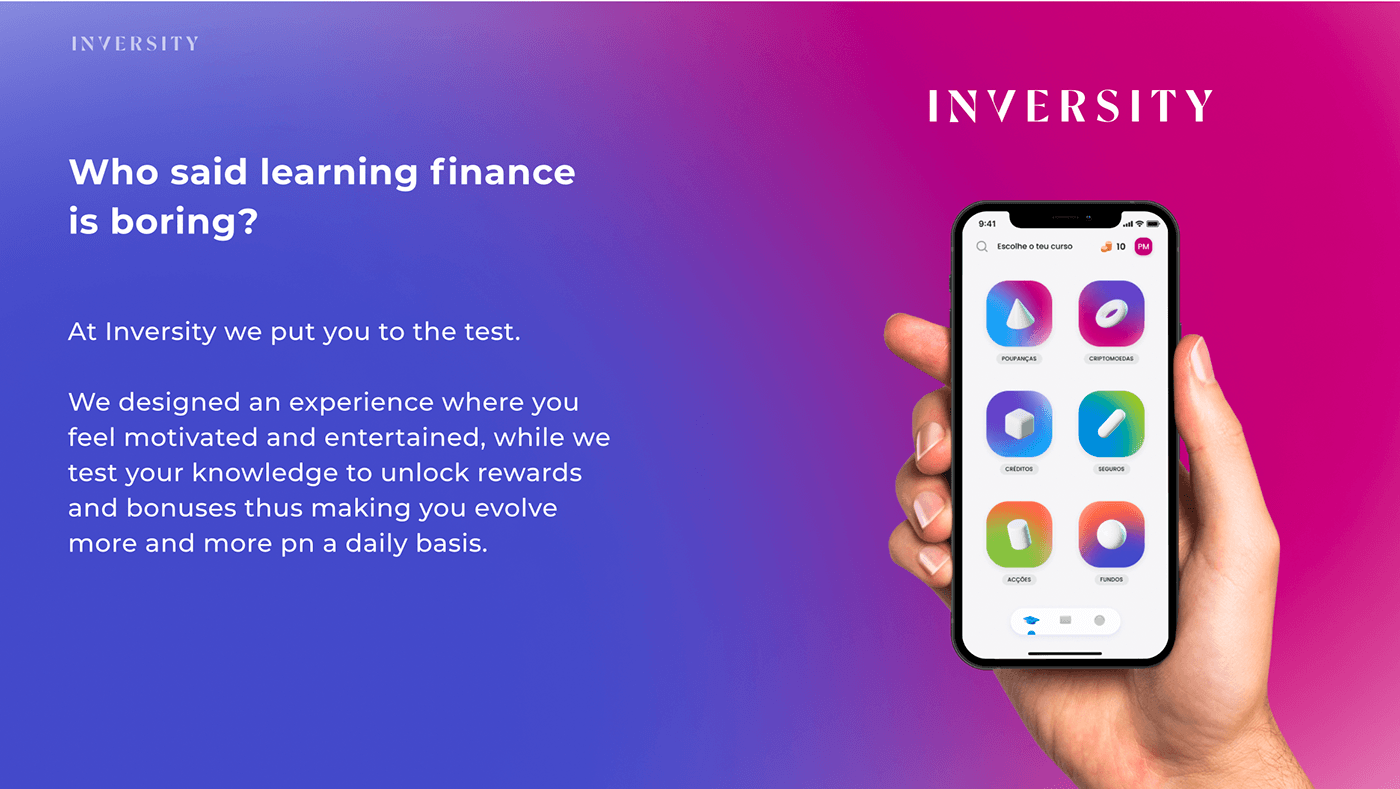

INVERSITY

Inversity is a service where EdTech meets Fintech, a ‘University of investment‘ that allows users to learn intuitively about the financial market, as well as giving them the possibility of actual investment , all in the same platform.

The gamification of knowledge is achieved through multiple UX practices conceived to maintain the user engaged in the learning process. However, product subscription is always optional.

As a starting point, the user's profile would be diagnosed based on his interests and level of financial knowledge. Then, specific learning paths would be suggested according to that data input.

Personalization is at the core of the whole experience, where the user is guided through different learning paths using gamification dynamics (ex: Duolingo). Based on the profile, the user will have the possibility to customize their experience, learning through different dynamics — text, images, audio and/or video.

Being rewarded with tokens for completed courses and with that being able to unlock new courses and knowledge is the core strategy of this service.

As users unlock learning paths and understand what they are learning, they receive tokens as rewards and become able to subscribe to financial products specifically designed to his or her unique profile.

DELIVER

Banking has a long history of being a “business of trust”. We want to create a service that is a “business of truth”, one that serves a demanding public that no longer accepts gate-keepers as regulators of their financial freedom.

Transparency is a fundamental value of what we are proposing, so the structure of Inversity would be based on a DAO community that gives its members the value of exchanging real-time knowledge, the possibility to access financial products from different banks or fintechs, and a Discord channel to talk and hang out with their communities and friends, while also sharing development and learning curves.

After analyzing different players, we concluded that the greatest value of Inversity is to combine learning with gamification, while allowing the user to invest in different financial products on the same platform.

Edtech meets Fintech is our motto and our will is to create a blue ocean service where all stakeholders win and everyone contributes to social financial literacy.

After our first prototype and several iterations, we tested our value proposition with users between 18 and 45+.

We used surveys and a Likert scale to evaluate if participants:

• Are already investing their money

• Want to invest money but don't know how

• Feel that Inversely solves an actual problem

• Would use Inversely to learn about financial literacy and investing

• Would be willing to subscribe to a premium profile

• Like being able to chose how to learn and progress, according to daily availability, and to be rewarded for fulfilling goals

We found that in almost all questions, more than 70% of participants responded with "agree" or "strongly agree" about the possibility of using Inversity in their daily lives to empower themselves financially. We received a lot of feedback on how to improve the experience and make it even more inclusive.

availability, and to be rewarded for fulfilling goals.

We found that in almost all questions, more than 70% of participants responded with "agree" or "strongly agree" about the possibility of using Inversity in their daily lives to empower themselves financially. We received a lot of feedback on how to improve the experience and make it even more inclusive.

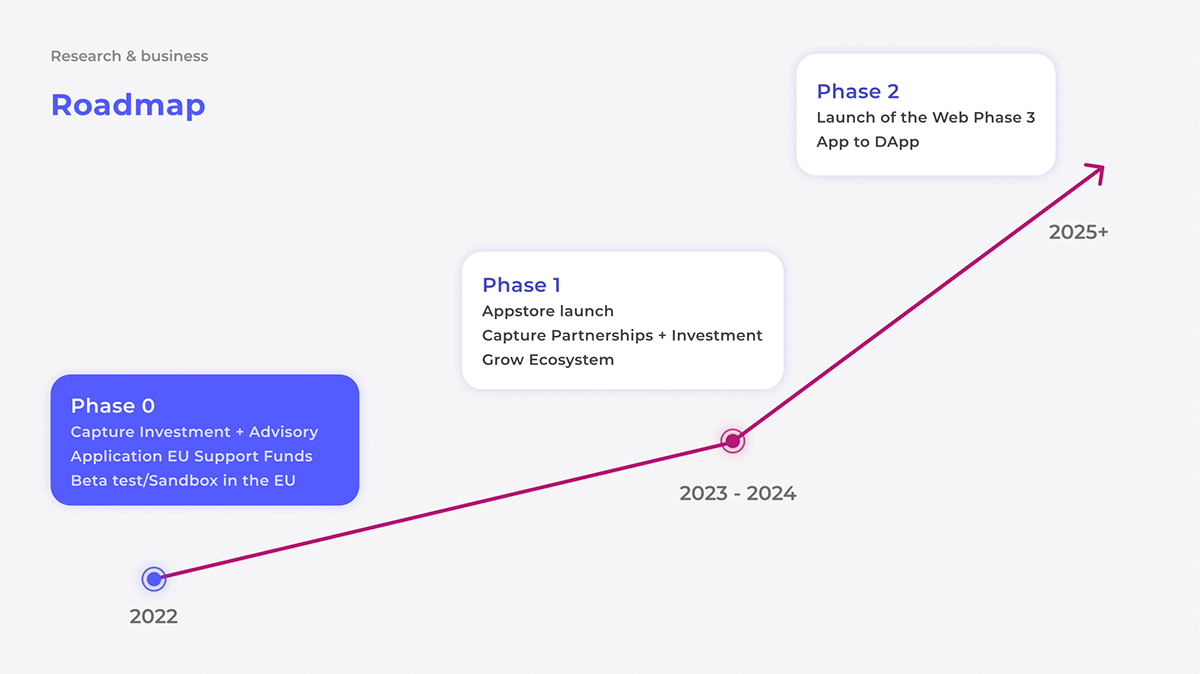

NEXT STEPS

The most interesting part of this whole journey was the process of understanding how we could become a bridge between financially disempowered people and a future where they enjoy the freedom to make their own choices.

We learned a lot about Open Banking and its possibilities, while understanding that financial services are on a path of profound transformation.

It goes without saying that the financial market is highly regulated and we are now in the process of improving our proposal by better understanding governance, risk management, and compliance issues specific to this field

We are now meeting with potential investors, experts in the field of banking, fintechs & investment, and mentors to help us unlock obstacles while ensuring we are not biased in our thinking.

All of our research, proof of concept and prototype tests give us real context to the main insight: there is a gap between current offering and market needs when it comes to enabling financial control and personalization.

Research has shown that there is high potential in creating a bridge between literacy and investment, both personalizing the relationship with the client and offering tailor-made products.

Inversity emerges as a platform that allows bridging this gap by creating a positive feedback loop, where gathered knowledge is rewarded while it generates more freedom to invest.

There is still work ahead but our purpose and values are clear:

We will help transform anyone into an investor. Our vision is a democratic future where every individual, regardless of context, feels empowered to make informed choices about financial decisions.

We will help transform anyone into an investor. Our vision is a democratic future where every individual, regardless of context, feels empowered to make informed choices about financial decisions.

Methodologies covered:

Desk Research / Interviews / Stakeholders Map/ Personas /

Empathy maps / Problem Statement Mapping / Value Proposition/ User Scenarios / User Flows / User Journeys/ Information Architecture/ Prototype/

Service Blueprint / Ecosystem Map / Business model canvas

Research Walls:

References:

1 OECD Studyhttps://www.oecd.org/financial/education/oecd-infe-2020-international-survey-of-adult-financial-literacy.pdf

2 Finastra Studyhttps://www.finastra.com/sites/default/files/2021-06/market-insight_ journey- financial-empowerment-global-report.pdf

I hope you enjoyed this project! Let me know in the comments.